Owner-Occupied vs. Investment Commercial Property Loans: Tax & Finance Differences 2026

When purchasing commercial property in Brisbane, one of the first decisions you’ll face is whether to acquire the property as owner-occupied or as an investment. Both options involve similar processes, but the financial and tax implications are significantly different. Explore our commercial property loans page to see how MC Mortgage Solutions can help you find the right financing solution. Understanding these differences is crucial for making the right decision for your business.

This guide will help you understand the distinctions between owner-occupied and investment commercial property loans. We’ll also provide insights into interest rates, tax benefits, deposit requirements, and lender policies. Additionally, we’ll explore how these factors impact your business and help you determine the most suitable loan type for your needs.

Owner-Occupied Commercial Property Loan vs. Investment Commercial Property Loan: What’s the Difference?

At the core, the key difference between owner-occupied and investment commercial property loans lies in the purpose of the property.

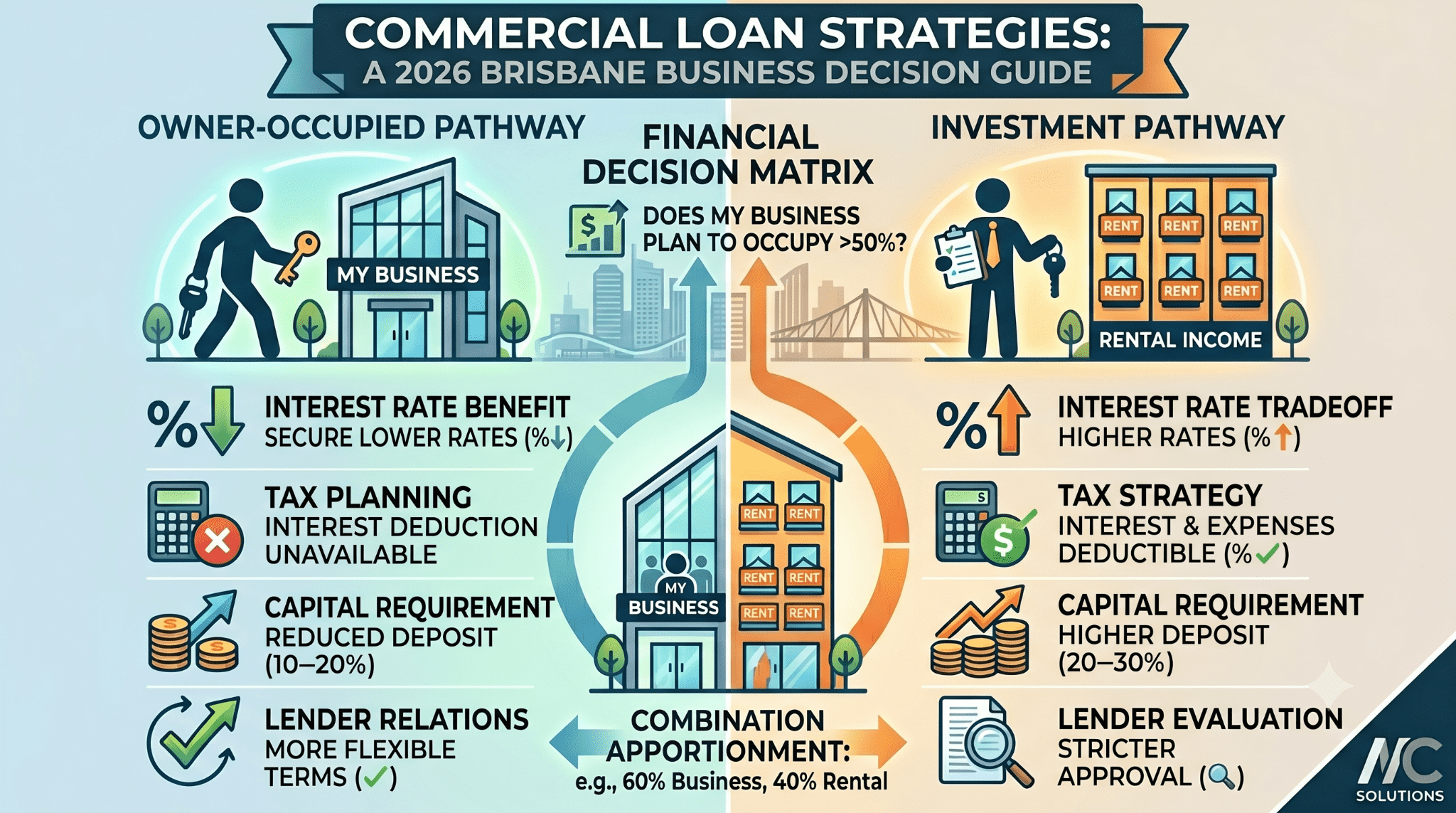

- Owner-Occupied Commercial Property Loans: These loans are for businesses that purchase property for their own use. If your business plans to occupy the property, either as an office, warehouse, retail space, or other commercial use, an owner-occupied loan is the best option.

- Investment Commercial Property Loans: On the other hand, investment loans are for businesses or individuals purchasing property to generate rental income. This could involve purchasing a building or retail space to rent out to tenants.

Understanding this distinction will help guide your decision-making process, as each loan type comes with its own benefits and restrictions.

Interest Rate Differences Between Owner-Occupied and Investment Loans

One of the most significant differences between owner-occupied and investment commercial property loans is the interest rate. Read our guide on variable vs fixed rate loans to understand how your rate structure can further impact your repayments over time.

- Owner-Occupied Loans: Lenders typically offer lower interest rates for owner-occupied loans. This is because the property is seen as a business asset that directly contributes to the company’s operations. Lower rates can translate into significant savings on your loan repayments over time.

- Investment Loans: Interest rates for investment loans are usually higher. This is because lenders view investment properties as more risky. There’s no direct benefit to the borrower other than the potential for rental income, which is less predictable.

Tax Deductions Comparison: Owner-Occupied vs. Investment Loans

Tax implications play a crucial role in determining the financial benefit of either loan type. Both owner-occupied and investment loans offer different tax strategies. Read our guide on positive and negative gearing pros and cons to understand how gearing strategies can complement your commercial property tax position.

- Owner-Occupied Loans: If you take out an owner-occupied commercial property loan, the interest paid on the loan is not deductible for tax purposes. However, if the property is used partially for business and partially for personal use (for example, a small retail store that also has living space), you may be able to claim a portion of the interest payments as a business expense.

- Investment Loans: With an investment property loan, you can generally deduct the interest paid on the loan as a business expense. You can also claim a range of other tax-deductible expenses associated with the investment property, including property management fees, repairs, depreciation, and even legal costs.

Deposit Requirements for Commercial Property Loans

When applying for a commercial property loan, the deposit requirement will vary depending on whether the property is owner-occupied or investment-based. Learn more about how borrowing ratios work in our guide — what is loan-to-value ratio (LVR)?

- Owner-Occupied Loans: For owner-occupied commercial property loans, lenders typically require a lower deposit — around 10–20% of the property’s value. This is due to the lower risk associated with the property being directly tied to your business.

- Investment Loans: Investment property loans usually require a larger deposit — often 20–30% of the property’s value. This is because investment loans are considered higher risk due to the uncertainty of rental income and the potential for vacancies.

It’s important to note that both types of loans may require additional security if the borrower’s credit history or financial situation isn’t strong enough to meet the deposit requirements.

Lender Policies & Restrictions

Lenders have different policies for owner-occupied and investment commercial property loans, which can affect your ability to secure financing and the terms they offer. Read our guide on national vs local mortgage lenders to understand which type of lender may suit your commercial property needs best.

- Owner-Occupied Loans: Lenders are generally more flexible when it comes to owner-occupied commercial property loans. Because the property will be used directly for your business, lenders see this as a safer bet. There may be fewer restrictions on loan terms, and in some cases, businesses can even secure loans with lower fees and fewer reporting requirements.

- Investment Loans: On the other hand, lenders tend to have stricter requirements for investment loans. You may face additional paperwork, such as providing proof of rental income, demonstrating the property’s rental potential, and undergoing a more detailed review of your business’s financial stability. Investment loans often come with more rigid loan-to-value (LTV) ratios, and the process may take longer due to the more thorough evaluation process.

Business Premises vs. Rental Investment: Choosing the Right Loan for Your Needs

The type of commercial property you’re buying will significantly influence your decision to choose between an owner-occupied or investment loan.

- Business Premises: If your business plans to occupy the property as part of your daily operations (e.g., office space, retail store, warehouse), you’ll need an owner-occupied loan. This makes sense because the property is a critical asset in running your business and contributes directly to your operational success.

- Rental Investment: If you’re purchasing property to generate income through renting, an investment loan is more appropriate. With rental properties, the primary goal is to secure a steady stream of rental income, so the loan is seen as an income-generating asset rather than a business tool.

Combination Loans: Owner-Occupied and Investment Mix

In some cases, businesses might need both owner-occupied and investment property features. For example, a business might purchase a commercial property where they occupy part of it and lease out the remaining space. In such cases, you can opt for a combination loan, which allows you to divide the loan into two parts: one for the owner-occupied section and one for the rental portion. Find out do mortgage brokers get better rates? and how working with a broker can help you structure the most competitive combination loan for your needs.

This type of loan allows you to enjoy the benefits of both loan types lower interest rates on the owner-occupied portion and tax-deductible interest on the investment portion. However, this can require more paperwork and a clear distinction between the business and rental areas within the property.

Brisbane Commercial Property Examples

Let’s consider some real-life scenarios where these loans could apply in Brisbane:

- Owner-Occupied Loan Example: A local tech startup might need office space in Fortitude Valley. The company purchases a commercial property for $800,000 with a 15% deposit. The lower interest rates make this an attractive option, especially considering the property is directly tied to their business’s success.

- Investment Loan Example: A property investor purchases a commercial retail space in South Brisbane for $1 million, planning to rent it out to tenants. With a 25% deposit and higher interest rates, the investor is looking at a longer-term income strategy, benefiting from rental returns and tax deductions on property-related expenses.

Tax Strategies with MC’s Accounting Service

Navigating the tax landscape when it comes to commercial property loans can be tricky, especially when determining which deductions apply to your specific situation. That’s where MC’s Accounting Service can assist. Explore our accounting services to see how MC Mortgage Solutions can help you maximise your commercial property tax benefits.

By partnering with an expert accountant, you can develop tax strategies that maximise your deductions, ensure compliance with local regulations, and ultimately save your business money. From structuring your loan to optimising property-related tax benefits, MC’s accounting service can help guide you through the complexities of owning commercial property, whether it’s owner-occupied or investment-based.

FAQs

An owner-occupied commercial property loan is a loan used to purchase a property that the borrower will use for their business operations, such as an office, retail space, or warehouse.

An investment commercial property loan is used to purchase properties for rental income purposes. The loan is structured around the potential income the property will generate.

Yes, you can use an owner-occupied loan for a mixed-use property, but the portion used for business must exceed the portion used for residential purposes to qualify.

Yes, interest rates are generally higher for investment property loans because they are considered riskier by lenders compared to owner-occupied loans.

Tax benefits for investment properties typically include deductions for interest paid on the loan, property management fees, repairs, and depreciation of the building and assets.

For owner-occupied commercial loans in Brisbane, deposit requirements typically range from 10–20%, while investment loans may require a deposit of 20–30% depending on the lender.

Yes, refinancing an investment commercial property loan is possible, and it may be a good option to secure better interest rates or more favourable terms.

Owner-occupied loans tend to have higher LTV ratios, often up to 80–90%, while investment loans typically have lower LTV ratios due to the higher risk involved.

Some government programs, such as the First Home Loan Deposit Scheme, may offer assistance for businesses purchasing their own premises. However, these are more common for residential loans than for commercial properties.

Yes, part of an owner-occupied property can be rented out, but the loan will still be considered owner-occupied as long as the majority of the property is used for business operations.

Conclusion

Deciding between an owner-occupied commercial property loan and an investment commercial property loan depends on your business goals and financial situation. Understanding the differences in terms of interest rates, tax deductions, deposit requirements, and lender policies will help you make an informed decision.

Whether you’re looking to purchase a property to house your business or to generate rental income, ensuring you choose the right loan type is critical to securing the best deal. Take advantage of the various tax benefits, and consider how a combination loan might be a viable option if you need both business premises and investment space. Don’t hesitate to contact MC Mortgage Solutions today — our team is ready to guide you through the decision-making process and help you make the most of your commercial property investment.